International DIY News

Kingfisher: Polish Sales Increase; Strong Growth In Iberia

Kingfisher plc has published a trading update for the 2024/2025 financial year.

Click here for the full results summary

Click here for UK & Ireland results

Click here for France performance

POLAND

Poland sales increased by 3.2% (LFL -0.1%) to £1,788m, supported by a stable consumer environment and market share gains (as measured by GfK) following strong progress in the development of initiatives to drive trade customer sales. ‘Big-ticket’ categories delivered LFL growth YoY, driving a sequential improvement in overall sales in H2 vs H1. ‘Big-ticket’ sales growth in Q4 was largely driven by the bathroom & storage category following improvements to the customer journey and marketing. Underlying core and seasonal category sales both improved in H2, with strong growth in Q4 driven by trade customer sales. Castorama’s e-commerce sales increased by 4.3% YoY, supported by improved technology and stronger sales from its mobile app. Castorama successfully launched its e-commerce marketplace in January 2025, with positive early results. E-commerce sales penetration was 3% (FY 23/24: 3%; FY 19/20: 2%). The business continues to focus on developing its trade customer proposition through further roll-out of ‘CastoPro’ zones, now in 12 stores, and 54 specialised sales partners now in 40 stores. The business launched an app for its trade customers in December, with c.75k downloads since launch. Trade sales penetration reached 24.5% in January, up 19.1%pts since the start of FY 24/25.

Space growth contributed c.3.3% to total Poland sales. Castorama opened five stores in the year (four big-boxes and one compact ‘Castorama Smart’ store), bringing its total to 107 stores in Poland as of 31 January 2025.

Gross margin % increased by 80 basis points, reflecting the effective management of product costs, supplier negotiations and retail prices, partially offset by higher promotional participation, clearance, and category mix. Retail profit increased by 8.0% to £90m (FY 23/24: £82m, at reported rates), with a higher gross profit partially offset by higher operating costs. Operating costs increased by 5.4%, reflecting the YoY increase in pay rates, higher staff bonuses, and higher costs associated with five new store openings. Cost increases were partially offset by savings achieved by our structural cost reduction programme, and the flexing of staff levels and discretionary spend. The operating costs movement also reflects a favourable YoY impact from charges related to ineffective foreign exchange hedges in the prior year. Retail profit margin % increased by 20 basis points to 5.1% (FY 23/24: 4.8%, at reported rates).

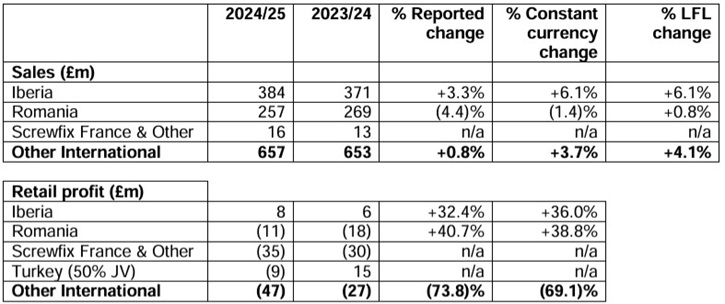

OTHER INTERNATIONAL

Other International total sales increased by 3.7% (LFL +4.1%) to £657m, driven by strong growth in Iberia. Retail loss increased to £47m (FY 23/24: £27m retail loss, at reported rates). This reflected losses in Turkey and Screwfix France & Other, partially offset by higher retail profits in Iberia and a reduced loss in Romania.

Iberia total sales increased by 6.1% (LFL +6.1%) to £384m. Sales trends were strong in H2 (LFL +10.6%) vs H1 (LFL +2.3%), with double-digit LFL sales growth in Q4 of core and ‘big-ticket’ categories. Seasonal sales were down for the year overall, though were much stronger in H2 (LFL +5.7%). The business saw encouraging results from the continued development of its trade customer proposition, resulting in doubledigit YoY sales growth in its building & joinery category. Brico Dépôt also continued to scale its ecommerce marketplace, reaching an e-commerce sales penetration of 33% in January 2025. Retail profit increased to £8m (FY 23/24: £6m, at reported rates), reflecting higher gross profit partially offset by higher operating costs (up 8.2% YoY).

Romania total sales decreased by 1.4% (LFL +0.8%) to £257m. Sales trends slowed in H2 (LFL +0.1% vs H1 +1.5%), with much improved core and ‘big-ticket’ sales offset by the impact of unfavourable weather on seasonal category sales. The business achieved LFL sales growth in its building & joinery, bathroom & storage, outdoor and tools & hardware categories in the year. Romania’s retail loss decreased to £11m (FY 23/24: £18m reported retail loss), reflecting slightly higher gross profit and lower operating costs. Operating costs decreased by 5.6%. In December 2024, we announced the sale of the entire Brico Dépôt Romania business including its network of 31 stores, distribution operations and head office to Altex Romania, for an enterprise value of €70m (equivalent to c.£58m). The sale is expected to complete in H1 25/26.

Screwfix France & Other consists of the consolidated results of Screwfix France, NeedHelp, and franchise and wholesale agreements. In line with our expectations, a combined retail loss of £35m (FY 23/24: £30m reported retail loss) was recorded, largely driven by Screwfix France as the business invested in the opening of new stores. Screwfix had a total of 30 stores in operation in France as of 31 January 2025, opening 10 new stores in the year. The business continues to see encouraging sales trends against the backdrop of market weakness in France, and remains focused on strengthening its brand awareness in the north of France (up three percentage points YoY) and further developing its customer proposition, including growing its Screwfix Sprint proposition and campaigns to attract and retain trade customers. Screwfix plans to open up to five stores in France in FY 25/26. On 18 July 2024, we completed a divestment of our c.80% equity interest in NeedHelp. Finally, we are focused on growing our franchise and wholesale business in new markets. We currently have six wholesale partners across 10 countries in Europe, Africa and the Middle East, whereby certain own exclusive brands (OEB) products are supplied to retailers.

In Turkey, Kingfisher’s 50% joint venture, Koçtaş, contributed a retail loss of £9m (FY 23/24: £15m retail profit, at reported rates) in a highly challenging and volatile macroeconomic and trading environment.

Including our share of Koçtaş’ interest and tax (FY 24/25: £6m loss vs FY 23/24: £16m loss), the overall contribution of Koçtaş to Group adjusted PBT was a net loss of £15m (FY 23/24: £1m net loss). This net loss was better than our expectations, primarily due to lower than anticipated hyperinflation adjustments. The financial performance largely reflects sales challenges, in addition to higher operating costs related to staff pay rates and costs of credit collection, together with the negative impact of accounting under high inflation. As a result of these challenges, Koçtaş swiftly initiated a comprehensive restructuring programme in the year, including a large reduction in headcount (c.900 FTEs) and the net closure of 106 stores. As of 31 January 2025, the business had a total of 262 stores in Turkey.

Source : Kingfisher

Insight provides a host of information I need on many of our company’s largest customers. I use this information regularly with my team, both at a local level as well as with our other international operations. It’s extremely useful when sharing market intelligence information with our corporate office.

Don't miss out on all the latest, breaking news from the DIY industry