UK DIY News

Kingfisher Reports 'Resilient' Interim Performance

Kingfisher PLC has published unaudited half year results for the six months ended 31 July 2022.

Highlights

- H1 performance in line with expectations (total sales -2.8% in constant currency and LFL -4.1%)

- Sales significantly ahead of pre-pandemic levels (3-year LFL sales +16.6%), supported by market share gains; Group Q2 sales trend ahead of Q1

- Resilient sales from both DIY and DIFM/trade categories

- Continued effective management of inflation and supply chain pressures

- Strong execution against our strategic priorities and investing for growth - digital, trade proposition, Screwfix and Poland expansion

- Attractive shareholder returns through dividends and ongoing second £300m share buyback programme; reflects confidence in long-term growth and cash generation opportunity

Thierry Garnier, Chief Executive Officer, said:

"Kingfisher has delivered a very resilient first half of sales. While facing very strong comparatives from the prior year as well as a more challenging environment, LFL sales were 16.6% ahead of pre-pandemic levels with a sequential improvement from Q1 to Q2. This was driven by the extension of share gains in all our key markets, reflecting successful execution of our strategy, and resilient sales from both DIY and trade customers. We are now back to pre-pandemic levels for in-store product availability and maintaining competitive pricing across our banners.

"Looking to the months ahead, although trading in the year to date has been in line with our expectations, we remain vigilant against the more uncertain economic outlook for the second half. We are therefore focussed on delivering value to our customers at a time when they need it most. You can expect continued strong execution, with a focus on growing sales and market share, effective management of our gross margin, and alignment of our costs and inventories to market conditions.

"With the business and our balance sheet in a strong position, we continue to invest in opportunities to drive growth. B&Q successfully launched its first home improvement marketplace during the period, and we are now preparing for marketplace launches in France, Poland and Iberia. We are also continuing to invest in the trade segment through Screwfix's expansion in the UK and Ireland, as well as the further development of our offer for tradespeople across our banners, building on the success of TradePoint. We are on course to open our first Screwfix stores in France within a few weeks from now. And we are developing innovative new products and services to support more sustainable and energy efficient homes, which will benefit our customers and the environment.

"These investments, together with the proven resilience of the home improvement sector, our balanced exposure to DIY and DIFM/trade, and our strong and consistent execution, support our confidence in continuing to grow ahead of our markets."

H1 22/23 Group results

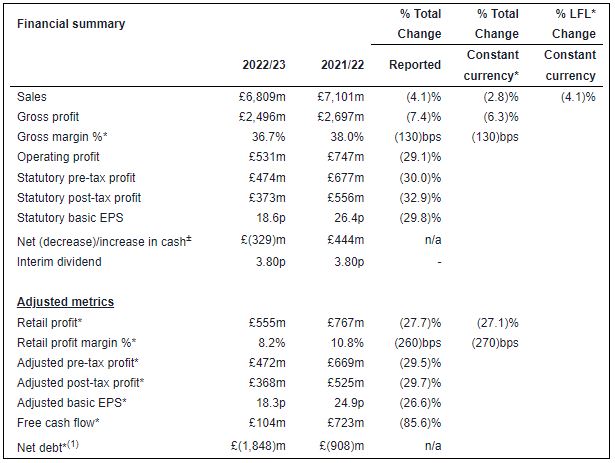

- Sales down 2.8% in constant currency, reflecting strong prior year comparatives linked to high demand for home improvement products. Resilient sales across both retail and trade channels

- LFL sales down 4.1% and corresponding 3-year LFL* up 16.6%

- Double-digit 3-year LFL sales growth across all banners (i.e., versus pre-pandemic levels)

- Positive 1-year growth in Poland, Iberia* and Romania; resilient performance in France*; strong prior year comparatives for the UK & Ireland*

- Q2 22/23 LFL sales up 17.4% on a 3-year basis, adjusted for a c.0.7% adverse calendar impact; stronger trend than Q1 22/23 (+14.8%, adjusted for a c.1.4% positive calendar impact)

- Total e-commerce sales* down 19% (3-year growth up 156%); new B&Q marketplace proposition performing well, and omni-channel customer engagement scores remain high

- E-commerce sales penetration* of 16% (H1 21/22 and H1 19/20: 19% and 7%, respectively)

- B&Q marketplace gross sales* performing ahead of expectations, representing 8% of B&Q's total e-commerce sales in August 2022

- Gross margin % down 130 basis points to 36.7% (H1 21/22: 38.0%; H1 19/20: 37.0%), reflecting an exceptionally strong prior year comparative ('normalised' promotional activity versus the prior year, one-off logistics spend to secure/manage seasonal and 'buffer' stock, and banner & category mix)

- Retail profit down 27.1% in constant currency to £555m (H1 21/22: £767m; H1 19/20: £454m), largely reflecting very strong prior year comparatives in the UK & Ireland

- Statutory pre-tax profit down 30.0% to £474m (H1 21/22: £677m; H1 19/20: £245m), reflecting lower operating profit, partially offset by lower net finance costs

- Adjusted pre-tax profit down 29.5% to £472m (H1 21/22: £669m; H1 19/20: £337m), reflecting lower retail profit, partially offset by lower net finance costs

- Free cash flow of £104m, down 85.6% (H1 21/22: £723m; H1 19/20: £204m), largely reflecting working capital outflow associated with completion of inventory rebuild programme

- Net decrease in cash of £329m (H1 21/22: net increase in cash of £444m), largely reflecting lower free cash flow, and £390m of outflows in relation to ordinary dividends and share buybacks

- Net debt of £1,848m (£1,572m as of 31 January 2022), reflecting the net decrease in cash

- Net debt to last twelve months' EBITDA* of 1.3x (1.0x as of 31 January 2022)

- Interim dividend per share declared of 3.80p (FY 21/22 interim dividend: 3.80p)

Outlook for FY 22/23

- An encouraging start to trading in the second half of the year:

- Q3 22/23 LFL sales (to 17 September 2022)(2) up 15.2% on a 3-year basis, with 1-year LFL down 0.7%

- Continued resilience in outdoor and 'big-ticket' category sales trends

- H1 performance and current trading in Q3 consistent with FY 22/23 adjusted pre-tax profit guidance of c.£770m, as set out at the start of this year

- For the balance of year, we have run several trading scenarios to take into account the potential for a more uncertain macroeconomic environment. These point towards a range of outcomes for FY 22/23 adjusted pre-tax profit(3) of c.£730m to £770m

- Expect continued strong execution:

- Targeting further market share growth

- Anticipate full year gross margin % to be in line with pre-pandemic level (FY 19/20: 37.0%)

- Accelerating investment in Screwfix France

- Committed to continued active and responsive management of our operating costs*

- Anticipate reduction of stock levels in H2 related to sell-through of a large part of 'buffer' stock previously held to protect product availability

Continuing to deliver against our strategic priorities

- Strengthened competitive position in all key markets

- High revenue retention rates of customers acquired during the pandemic

- France: on track to complete 'fixes' in H2; LFL growth above market and priority to deliver more profitable growth

- Focused on investments to support long-term growth: Investing in faster fulfilment and expanded product choice; targeting further store expansion in Screwfix UK & Ireland and Castorama Poland; opening first Screwfix stores in France within weeks; stepping up initiatives to further increase trade penetration across the Group

- E-commerce:

- Expanded store-based picking model for faster click & collect (C&C) and last-mile delivery, including optimised order management through 'digital hub' stores, roll-out of C&C lockers in Poland (also being tested at B&Q) and continued successful roll-out of one-hour delivery with Screwfix Sprint

- New e-commerce marketplace model successfully launched at B&Q (100,000 SKUs* added in six months); preparing roll-out of marketplaces in France, Poland, Spain and Portugal

- Own exclusive brands (OEB):

- OEB driving affordability, sustainability and wider customer engagement

- OEB represented 45% of Group sales in H1 (H1 21/22: 46%); strong performance in kitchen, bathroom & storage and EPHC (electricals, plumbing, heating & cooling) categories

- Developing specific OEB for different retail banners and extending ranges to support choice - roll-out of 32 new and redeveloped OEB brands almost complete

- Mobile-led and service innovations:

- Embedding Scan & Go into the B&Q app

- Extending the roll-out of self-checkout terminals across B&Q, Castorama France and Poland

- Extended 3D design tool capabilities to new categories (including bathrooms, modular storage solutions, fireplaces)

· Compact stores and rightsizing:

- Continuing to test new compact stores and partnership models; opened six new compact stores in H1 in the UK, France and Poland, and first two B&Q franchise stores in the Middle East

- Positive initial results from the five stores rightsized in the UK and France last year; preparing for further rightsizings in H2 (in line with our previously announced target of up to 40 'big-box' store rightsizings across B&Q and Castorama France over 10 years)

- Trade proposition:

- A record 31 new store openings for Screwfix in the UK & Ireland in H1

- Screwfix online sales in France continue to perform well; first distribution centre now operational, supporting opening of first stores in France within a few weeks from now

- TradePoint (in B&Q) 3-year LFL sales growth of 34%, outperforming core B&Q and Screwfix, and reaching 21% sales penetration

- Launched plan to grow trade customer penetration across all 'big box' banners, including new trade loyalty programmes in Poland and Iberia, and the introduction of new OEB and branded trade-focused ranges

- Costs and inventory:

- Multi-year cost reduction programmes partially mitigating against inflation pressures

- Majority of year on year (YoY) increase in net inventory driven by inflation (61%) and store expansion (7%)

- Proactive inventory purchases from Q4 last year to (i) rebuild product availability, (ii) build seasonal and 'buffer' stock ahead of peak trading, and (iii) secure lower cost stock,

- Actions underway to further optimise sourcing footprint and maximise Group sourcing efficiencies

- Good inventory health, with stock provisioning rates below pre-pandemic levels

- Responsible Business:

- Announced new net-zero emissions target for our operations (scope 1 and 2) by the end of 2040

- Innovative end-to-end solutions at B&Q and Brico Dépôt France to help customers create a personalised energy efficiency action plan for their homes, including access to relevant products and services

- New targets for growth of sustainable home product sales

Source : Kingfisher PLC

Image : Alan Morris / iStockphoto.com (1281594226)

Insight DIY is the only source of market information that I need and they always have the latest news before anyone else.

Don't miss out on all the latest, breaking news from the DIY industry