UK DIY News

Grafton Group 'Confident' Despite Revenue Decline

Grafton Group plc (“Grafton” or “the Group”), the international building materials distributor and DIY retailer, issues this trading update for the period from 1 January 2024 to 30 June 2024 ahead of the release of the half year results on 29 August 2024.

Eric Born, Chief Executive Officer of Grafton Group plc commented:

“We were very pleased with the performance of our businesses in Ireland, where the outlook for growth continues to remain positive. Elsewhere the repair, maintenance & improvement, and new build markets remain more challenging, but our management teams will continue to actively manage both our gross margins and cost base in response to market conditions. Medium-term structural industry dynamics remain positive, and as flagged at the time of our AGM update in May, we expect profitability to be slightly more weighted to the second half of the year.

“Given our strong financial position we are actively progressing inorganic development opportunities in existing and new European geographies. Our objective is to continue to strengthen our market and sector positions and add to our portfolio of high-quality cash generative businesses within a disciplined financial framework.

“With our strong market positions and the scope for operating leverage throughout the Group’s businesses as the macro-economic outlook improves, we remain confident in the medium-term outlook for Grafton.”

Trading and Performance

Group revenue in the period from 1 January 2024 to 30 June 2024 was £1.14 billion (H1 2023: £1.19 billion), down 4.4 per cent from the prior year and 3.0 per cent lower in constant currency.

Overall trading in the Group’s businesses remained challenging in the period with average daily like-for-like revenue down 4.5 per cent on the prior year and our management teams have continued to actively manage both our gross margins and cost base in response to market conditions.

Distribution

In Ireland, Chadwicks saw a resumption of growth in average daily like-for-like revenue in the second quarter following a decline of 0.2 per cent in the first quarter of the year. Volume growth in the first six months of circa 5.4 per cent was strongly ahead of the comparable period last year. The Government policy agenda is strongly supportive of increasing the development of new homes and, as a consequence, the housing market continues to grow with commencements strongly ahead in the first half and reaching a post Global Financial Crisis high. The outlook for growth in construction in Ireland remains positive and the deflationary pressures seen in steel and timber have continued to moderate with overall price deflation of circa 4.9 per cent in the first six months.

In the UK, the weak trends experienced in the first quarter in the repair, maintenance & improvement market continued up until the end of the period. In Selco, price deflation in June was circa 2.0 per cent and is showing an improving trend from the rate of circa 4.0 per cent experienced in the first half overall. Customers remain cautious with discretionary spending which has resulted in lower investment on home improvements, although there are positive signs emerging of improving consumer confidence.

In the Netherlands, revenue growth from customers engaged on larger construction projects continued to partially offset the modest decline in sales to timber factories and smaller customers. There have been more positive signs that the housing market is starting to improve with increasing transactions and price rises in the existing housing stock.

In Finland, IKH’s average daily like-for-like revenue was 7.7 per cent lower as a result of the continued weakness in the domestic economy, export markets and the construction sector in particular, but it performed well against the overall Finnish market.

Retailing

In the Woodie’s DIY, Home and Garden business in Ireland, sales were slightly weaker in the second quarter, but good margin management and cost control has delivered an improvement in profitability over the same period last year.

Manufacturing

In UK Manufacturing, CPI Mortars continued to experience a decline in volumes in line with the fall in house building activity. In StairBox, the weakness in the RMI market resulted in lower volumes compared to the prior year but good margin management and the beneficial impact of the acquisition of TA Windows has contributed to an improvement in profitability compared to the same period last year.

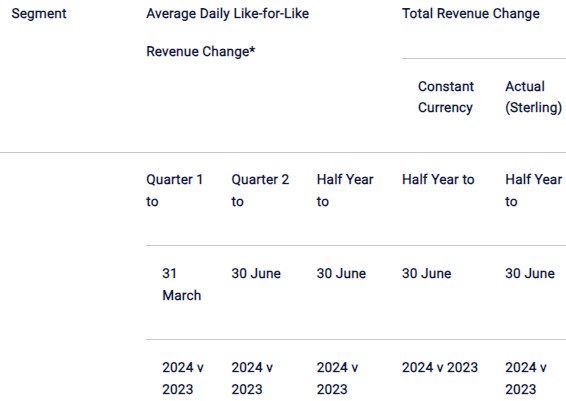

Segmental Trading

The table below shows the changes in average daily like-for-like revenue and in total revenue for the period from 1 January 2024 to 30 June 2024 compared to the same period in the prior year.

Source : Grafton Group plc

I find the news and articles they publish really useful and enjoy reading their views and commentary on the industry. It's the only source of quality, reliable information on our major customers and it's used regularly by myself and my team.

Don't miss out on all the latest, breaking news from the DIY industry